The form of the invoice used in the calculation of value added tax, and the rules for filling it out are enshrined in Decree of the Government of the Russian Federation of December 26, 2011 No. 1137.

From October 1, 2017 invoice form supplemented with the line "Product type code". This line must be filled in by companies that supply goods to the countries of the Eurasian Economic Union - Armenia, Belarus, Kazakhstan and Kyrgyzstan.

AT new form of invoice from 01.10.2017 there were changes in the filling. It is now necessary to indicate the addresses of the seller and the buyer in accordance with the Unified State Register of Legal Entities and the EGRIP. In addition, for imported goods, not a serial number, but a registration number of the customs declaration is entered. All changes are described in detail in the Decree of the Government of the Russian Federation of August 19, 2017 No. 981.

The procedure for filling out a new invoice form 2018-2019 on our website

In the Invoice No. field enter the serial number of the invoice. Our service supports auto-numbering, but we can also enter this value manually. Separate divisions, as well as partnerships and trustees, can supplement the main invoice number with their index through a separating line. In the "from" field - indicate the date of the document, while you can use the built-in calendar by selecting the required date in it.

In the field "Corrections" select the required value. When filling out the invoice for the first time, you should leave the default value “not entered”, in this case, a dash will be automatically inserted in the finished document in the “Correction” line. If you select the value “Introduced”, the fields “Correction #” and “from” will appear, in which you need to specify the serial number of the correction made to the invoice and the date this correction was made.

In the field "For advance payment" it is necessary to select the value “yes” if an advance invoice is being drawn up, i.e. upon receipt of payment, partial payment on account of the forthcoming deliveries of goods (performance of work, provision of services), transfer of property rights. At the same time, in the printed form of the invoice, dashes will be automatically entered in the lines “Consignor and his address” and “Consignee and his address”, as well as in columns 2-6, 10-11 of the tabular part of the document. If the invoice is issued together with closing documents upon the fact of shipment of goods, performance of work, provision of services, then this field should be left with the default value “no”.

In the "Document currency" field select the name of the currency that is the same for all goods (works, services) listed in the invoice, property rights, including non-monetary forms of payment. Its name and digital code will be reflected in the document in accordance with the All-Russian Classifier of Currencies. If the currency you need is not in the list, you can enter its name and code manually by selecting the “Other” value.

In the rows of the table "To the settlement and payment document" all numbers and dates of settlement and payment documents for which cash on the date of drawing up the invoice in payment for the goods, works, services listed in it.

In the "Seller Information" section you must select the value "Organization", if the invoice is a legal entity, or "IP". In the first case, it is necessary to fill in the fields with the following details: short or full name of the organization, detailed address in accordance with the Unified State Register of Legal Entities (zip code, city, street, house, office), TIN, KPP, full name of the head or authorized person, full name of the chief accountant (you can indicate the full name and initials). In the second case, in the fields you need to indicate the full name of the entrepreneur, the address from the USRIP (zip code, city, street, house, apartment), TIN and details of the state registration certificate.

In the "Consignor" section if the seller and the shipper are the same person, you need to select the value “He is the same” (in the printed form it will be reflected - “he is the same”); when drawing up an invoice for work performed (services rendered), property rights, it is necessary to put a “check box” in the value “Do not specify” (a dash will be put in the printed form); if the seller and the consignor are not the same person, you need to select the value "Third Party Organization" - for this case, the full or abbreviated name of the consignor organization in accordance with the constituent documents and its postal address must be entered in the appropriate fields.

In the "Customer Information" section in the field "Name" you need to indicate the full or abbreviated name of the buyer, in the field "Address" - the detailed address in accordance with the Unified State Register of Legal Entities or the Unified State Register of Enterprises, in the fields "TIN" and "KPP" - the individual number of the taxpayer-buyer and his registration reason code respectively. Individual entrepreneurs do not fill in the "KPP" field.

In the field "Identifier of the state. contract" the number assigned by the state is indicated. contract or agreement (agreement). The number of characters of the identifier can be different: 20 digits for the treasury support of the contract, 25 digits for the defense order. If the contract is normal, then the field is not filled.

In the "Consignee" section if the buyer and the consignee are the same person, you should select the value “He is the same” - the required lines in the printed form will be filled with information about the buyer; when drawing up an invoice for work performed (services rendered), property rights, you should select the value “Do not specify” - in this case, a dash will be put in the printed form; if the consignee and the buyer are different companies, it is necessary to select the value "Third party organization" - in this case, the full or abbreviated name of the consignee in accordance with the constituent documents and his postal address must be entered in the appropriate fields.

In the "VAT" section in the "VAT calculation" field, you must put a "checkbox" in one of the values. By choosing the calculation option "In total", in the tabular part of the form in the column "Price per unit" you should indicate the price, which already includes VAT; "Above" and "Do not take into account" - the price without VAT is indicated. For the cases "Total" and "Above", VAT calculation will be performed automatically. In the field "VAT rate" in the drop-down menu, select "20%" (until 01/01/2019 - "18%"), "10%" or "Without VAT" depending on your taxation system and the nature of the transaction.

In the tabular part, you need to sequentially fill in the columns:

- Name- the name of the supplied (shipped) goods (description of work performed, services rendered), property rights transferred;

- TN VED (Code of the type of goods)- filled in by companies that supply goods to the EAEU countries - Belarus, Armenia, Kazakhstan, Kyrgyzstan. The code of the type of goods is indicated in accordance with the unified Commodity Nomenclature for Foreign Economic Activity of the EAEU. If the company does not deal with such supplies, the field is not required.

- Units of measurement (code and symbol)- is selected in accordance with sections 1 and 2 OKEI of the All-Russian Classifier of Units of Measurement (OKEI); in the absence of indicators, it is not filled in - a dash will be put in the printed form;

- Quantity- the quantity or volume of goods supplied (shipped) under the invoice (work performed, services rendered), property rights transferred based on the accepted units of measurement; in the absence of indicators, it is not filled in - a dash will be put in the printed form;

- Unit price- price (tariff) per unit of measurement (if it is possible to indicate it) under the agreement (contract). Specified with or without VAT, depending on the value selected in the "VAT calculation" field; in the absence of indicators, it is not filled in - a dash will be put in the printed form;

- Sum- the cost of the entire quantity (volume) of goods supplied (shipped) according to the invoice (work performed, services rendered), property rights transferred - is calculated automatically;

- Country (code and short name)- filled in for goods whose country of origin is not the Russian Federation, are selected in accordance with the All-Russian Classification of the Countries of the World;

- No. GTD (registration number of the state customs declaration)- filled in for goods whose country of origin is not the Russian Federation.

Cost indicators are indicated in the currency declared in the “Document currency” field, while the data may not be rounded using kopecks, cents, etc.

The first copy of the invoice drawn up on paper is issued to the buyer, the second copy remains with the seller.

In invoices drawn up from the date of entry into force of the Government Decree Russian Federation dated December 26, 2011 No. 1137 on paper or in electronic form, corrections are made by the seller (including in the presence of notices drawn up by buyers on the clarification of the invoice in electronic form) by compiling new copies of invoices. In a new copy of the invoice, it is not allowed to change the indicators indicated in the fields “Invoice No., from” of the invoice drawn up before corrections were made to it, and the field “Correction No., from” is filled in, which indicates the serial number of the correction and the date fixes.

Errors in invoices that do not prevent the tax authorities from carrying out tax audit identify the seller, buyer of goods (works, services), property rights, the name of goods (works, services), property rights, their value, as well as the tax rate and amount of tax presented to the buyer, are not grounds for refusing to accept tax amounts for deduction (Clause 2, Article 169 of the Tax Code of the Russian Federation as amended by Federal Law No. 245-FZ of July 19, 2011)

The invoice is signed by the head and chief accountant of the organization or other duly authorized persons or an individual entrepreneur, indicating the details of the certificate of state registration of this individual entrepreneur.

Invoice - a document used to accept the presented amounts of VAT for deduction or reimbursement.

Invoices drawn up and issued in violation of the procedure established by the Tax Code of the Russian Federation cannot be the basis for accepting tax amounts presented to the buyer by the seller (and paid by the buyer) for deduction or reimbursement. Making additional requirements for filling out invoices is illegal, therefore, in order not to let down your buyers and customers, you should fill in the mandatory details of the invoice very carefully and accurately.

Mandatory details of the document are given in clauses 5 and 6 of Art. 169 of the Tax Code of the Russian Federation.

The invoice form is given in Resolution No. 194.

In order not to suspend the work of the head and chief accountant of the organization, the signing of invoices at large enterprises is entrusted to authorized persons by the relevant order.

In this case, instead of the surnames and initials of the head and chief accountant of the organization, after the signature, it is necessary to indicate the surname and initials of the person who signed the corresponding document. At the same time, if such an account also contains the surname and initials of the head and chief accountant of the organization, such a document should not be considered as drawn up in violation of the requirements of the Tax Code of the Russian Federation (letter of the Ministry of Finance of Russia dated July 26, 2006 No. 03-04-11 / 127).

Signatures must be original. Facsimile is not allowed.

The invoice can be certified by the seal of the organization. But this requisite is not mandatory, although a document certified by a seal commands more respect and reduces the likelihood of forgery.

If the invoice is issued by an individual entrepreneur (IP), then the details of the certificate of state registration of this entrepreneur must be indicated.

The absence in the document issued by the organization of the details "Individual entrepreneur" and "Details of the certificate of state registration by an individual entrepreneur", "Head of the organization" and "Chief accountant" is not a violation of the procedure for issuing invoices (letter of the Ministry of Finance of Russia dated July 26, 2006 No. No. 03-04-11/127).

The organization has the right to enter additional details in the invoice form. In this case, the modified form must be approved in the appendix to the order on accounting policies. At the same time, the sequence of location and the number of indicators of mandatory details should not change.

Invoices should not have erasures and blots. Corrections can only be made by the proofreading method. The corrective method is as follows: the incorrect text or amounts are crossed out and the corrected text or amounts are inscribed above the crossed out text. Strikethrough is done with one line so that you can read the corrected one. Corrections must be certified by the signature of the manager and the seal of the seller indicating the date the correction was made. In this case, we have a contradiction: the seal on the invoice itself is not a mandatory requisite, and the certification of corrections in it with a seal is mandatory (clause 29, section IV of Resolution No. 914).

For a long time, the question remained relevant: is it possible to deduct VAT on invoices filled out with the simultaneous use of typewritten and handwritten text? Despite the fact that arbitration courts have repeatedly recognized the legitimacy of deducting VAT on such accounts (decree of the Federal Antimonopoly Service of the North-Western District of July 16, 2002 in case No. A26-1327 / 02-02-058 / 35), tax officials often refuse to recognize such a VAT deduction. At the same time, the tax authorities themselves created confusion. Thus, the Deputy Head of the UMNS of Russia for Moscow, State Advisor to the Tax Service A.A. Glinkin issued two letters on this topic: July 24, 2001 No. 02-11/33627 and September 3, 2002 No. 24-11/40771. in the first letter, a mixed method of filling out invoices is allowed. In the second letter, all handwritten entries made to the typewritten invoice are recognized as corrections (the procedure for issuing corrections in invoices is described above).

On July 1, 2004, the Ministry of Taxes and Taxes of Russia for Moscow issued a letter No. 24-11/43467 on the procedure for filling out invoices, which is based on a private letter of the Ministry of Taxes of Russia dated February 26, 2004 No. 03-1-08/525/18. the letters clarified that "changing the external form of an invoice, including filling in an invoice combined (by computer and manually) should not violate the sequence of the location and number of indicators approved in the standard form of an invoice by Resolution No. 914." The Ministry of Finance of Russia supported the position of the tax authorities and issued a letter reflecting a similar opinion dated December 8, 2004 No. 03-04-11/217.

Amended by Decree of the Government of the Russian Federation of May 11, 2006 No. 283, the Rules were supplemented with a provision allowing registration in

2017

From July 1, 2017, the invoice form will change. See sample and form below. In the new line 8 “Identifier of the state contract, agreement (agreement)”, from July 1, 2017, it is necessary to indicate the identifier of the state contract for the supply of goods (performance of work, provision of services), agreement (agreement) on the provision from the federal budget legal entity subsidies, budget investments, contributions to the authorized capital.

Since 2017, registration certificates have not been issued. Instead of the details of the certificate of state registration of this individual entrepreneur, they enter data from the USRIP Record Sheet in the form No. Р60009.

General requirements

Invoice - the only document according to which it is possible to claim a VAT deduction (clause 1, article 172 of the Tax Code of the Russian Federation). cash receipt with the allocated amount of VAT will not work.

The Federal Tax Service launched the service "checking the correctness of filling in invoices" in test mode

An invoice can be issued even for transactions not subject to VAT (for example, with the simplified tax system). After all, the Tax Code gives the right not to issue an SF, but it does not prohibit this either, you just need to enter "Without VAT" (letter dated November 7, 2016 No. 03-07-14 / 64908).

In the invoice for goods, it is not necessary to include services for their transportation (Letter of the Ministry of Finance dated April 13, 2016 No. 03-07-09 / 21127).

If you need to cancel the invoice (for example, the document was issued prematurely), then the customer needs to write a letter stating that the invoice was issued erroneously. To cancel an entry in the (corrective) invoice, you must use the new pages in the purchase book for the quarter in which you made the incorrect entry. (Letter dated December 26, 2016 No. 03-07-09/77996).

The invoice must be issued within 5 working days after shipment or service. The day of shipment is also included in this period (letter of the Ministry of Finance dated 10/18/2018 No. 03-07-14 / 74899).

If prepayment and shipment of goods occur within 5 calendar days, i.е. occur in one tax period, the seller may not issue an advance invoice (the Ministry of Finance of Russia in a letter dated November 10, 2016 No. 03-07-14 / 65759).

Suppliers and buyers have different approaches to calculating VAT. The supplier calculates VAT on the dates when all advances are received and shipment occurs. The buyer also reflects VAT on the dates indicated in the invoices (you can also reflect the invoices of the reporting quarter received after the end of the quarter but before the declaration is submitted).

Replace the primary with an error with a new one prohibited by the accounting law. Corrections need to be made. (Letter of the Ministry of Finance dated October 23, 2017 No. 03-03-10/69280).

Electronic

The invoice must be issued either both copies in electronic form, or both copies in paper form. It is unacceptable for one person to have an electronic copy and the other to have a paper copy.

blank blank

advance invoice. For the absence of an advance invoice, inspectors can fine the company for 10 thousand rubles. If these documents have not been drawn up for two or more quarters - 30 thousand rubles. If the seller ships the goods within 5 days, then an advance invoice is not issued (clause 3 of article 168 of the Tax Code of the Russian Federation, letter of the Ministry of Finance of Russia dated January 18, 2017 No. 03-07-09 / 1695).

You can automate the process with . 30 days there for free, you can generate documents at this time. Generate and report on VAT via the Internet.

How should separate units be issued?

Separates must issue invoices on behalf of the parent organization and at the same time indicate their checkpoint in line 2b "TIN / KPP of the seller" (Letter of the Ministry of Finance dated 05/18/2017 No. 03-07-09 / 30038).

Line 1 "SF date"

The date of the invoice must be no earlier than the date of the source document.

Line 1a "Number and date of correction"

The line is filled in only in the case of drawing up a corrected invoice: the line indicates the serial number and date of correction. If no corrections are made to the invoice, then a dash is put in this line.

Line 2 "Seller"

Based on the constituent documents, an abbreviated or full name of the legal entity - the seller is entered, for an individual entrepreneur - full name.

Line 2a "Address"

Based on the constituent documents, the location of the legal entity - the seller is entered, for an individual entrepreneur - the place of residence. From October 1, 2017, the address must be taken from the USRIP or USRLE (), and not from the constituent documents. By the way, the address can be abbreviated "st." "G." etc. (Letter of the Ministry of Finance of October 20, 2017 No. 03-07-14/68778).

Line 2b "TIN / KPP of the seller"

Enter the taxpayer identification number, as well as a code explaining the reason for registering the taxpayer-seller

Line 3 "Consignor"

If Seller and Shipper are the same person, "same" is entered. If the invoice is drawn up by a tax agent or for the performance of work (rendering a service), a dash is put in this line.

Line 4 "Consignee"

Full or abbreviated name, address, in accordance with the constituent documents. If the invoice is drawn up by a tax agent or for the performance of work (rendering a service), a dash is put in this line.

Employees who signed the invoice can indicate their positions in them. By the way, the address can be abbreviated "st." "G." etc. (Letter of the Ministry of Finance of October 20, 2017 No. 03-07-14/68778).

Line 5 "To the payment and settlement document"

If the invoice is drawn up upon receipt of payment, partial payment against future deliveries using a non-monetary form of payment, a dash is put in this line.

Line 7 "Currency"

Digital code for OK currencies (Resolution of the State Standard of Russia of December 25, 2000 N 405-st). If payment under the contract is provided for in rubles in an amount equivalent to a certain amount in foreign currency or cu, then the ruble and its code 643 are indicated as the name of the currency. Important! In c.u. invoice cannot be generated. Euro 978, US dollar - 840

AT new line 8 "Identifier of the state contract, agreement (agreement)" from July 1, 2017, it is necessary to indicate the identifier of the state contract for the supply of goods (performance of work, provision of services), an agreement (agreement) on the provision of subsidies from the federal budget to a legal entity, budget investments, contributions to the authorized capital. If you do not have data about the identifier, then the line can be left empty (letter of the Ministry of Finance of Russia dated 08.09.2017 No. 03-07-09 / 57870).

Counts:

Column 1 "Name of goods"

Enter the name of the goods (shipped or supplied), description of the services rendered or work performed, transferred property rights. If partial or full payment has been received for the forthcoming delivery of goods (rendering services, performance of work), transfer of property rights, then write the name of the goods supplied, a description of services and work, property rights. The name in a foreign language is not allowed (letter of the Federal Tax Service of December 10, 2004 No. 03-1-08/2472/16). Although the Ministry of Finance believes that the Name of the product may be in a foreign language (Letter of the Ministry of Finance of the Russian Federation dated May 18, 2017 No. 03-01-15 / 30422) it is better to translate into Russian.

Column 1a "Product type code"

Since October 1, 2017. Only those companies that export (export) goods to Belarus, Kazakhstan, Armenia or Kyrgyzstan are filled in (Decree No. 981 dated August 19, 2017).

Column 2 "Code"

Column 2 and 2a is filled in in accordance with OK 015-94 (MK 002-97). "All-Russian classifier of units of measurement" (approved by the Decree of the State Standard of the Russian Federation of December 26, 1994 N 366).

Column 2a "Unit of measurement"

Column 3 "Quantity (volume)"

In the absence of an indicator, a dash is placed. Upon receipt of payment or partial payment, a dash is placed on account of upcoming deliveries.

Column 4 "Price (tariff) per unit of measurement"

In the absence of an indicator, a dash is placed. Upon receipt of payment or partial payment, a dash is placed on account of upcoming deliveries.

Column 5 "Cost of goods"

Column 3 multiplied by column 4.

Column 6 "Including the amount of excise duty"

In the absence of an indicator, an entry “without excise duty” is made. Upon receipt of payment or partial payment, a dash is placed on account of upcoming deliveries.

Column 7 "Tax rate"

You can automate the process with . 30 days there for free, you can generate documents at this time. Generate and report on VAT via the Internet.

Column 8 "Amount of tax presented to the buyer". The amount of VAT tax cannot be entered here with rounding. Need a penny.

Column 5 multiplied by column 7. For transactions listed in paragraph 5 of Article 168 of the Tax Code of the Russian Federation, an entry "without VAT" is made.

Column 9 "Cost of goods (works, services), property rights with tax - total" The amount of VAT tax cannot be entered here with rounding. Need a penny.

The sum of columns 5 and 8.

Box 10 "Country of origin"

To be filled in if the country of origin is not Russia. Upon receipt of payment or partial payment, a dash is placed on account of upcoming deliveries. To be filled in in accordance with the All-Russian Classification of the Countries of the World.

Column 10 "Digital code"

Column 10 and 10a is filled in in accordance with the OK of the countries of the world (MK (ISO 3166) 004-97) 025 - 2001.

Column 11 "Number of the customs declaration"

To be filled in if the country of origin is not Russia. Upon receipt of payment or partial payment, a dash is placed on account of upcoming deliveries.

Rules for filling out an invoice used for value added tax calculations (show/hide)II. Rules for filling out an invoice used in the calculation of value added tax

1. The lines indicate:

Corrective invoice

Download the blank form of the corrective invoice new form 2016-2017 32 kb. Excel (xls).

Download a blank form of a corrective invoice new form from July 1, 2017 38 kb. Excel (xls).

Suspicious for tax

Tax authorities can withdraw expenses or deductions based on signs:

- Product prices are too low or too high.

- The truck transported more goods than it can according to the technical passport.

- Goods are transported in an inappropriate route.

- Employees of the contractor/seller/buyer did not appear at the transaction/facility when it was necessary.

- The organization has prepared documents for verification for its counterparty (indicates that the organizations are interdependent).

- The organization prepared too many documents (suspicious).

When selling its products, the paying company must include the appropriate amount of value added tax (VAT) in the invoice. Invoice - document financial statements owing to which the company can accept this tax for reimbursement or deduction.

Such an opportunity is given only by a correctly filled out form in accordance with the established form.

The procedure for issuing invoices in 2019

An invoice is required in case of payment of VAT to the state. Firms that are not VAT payers do not issue it.

According to the law, the countdown starts from the moment:

- receipt by the buyer of the goods;

- payment for these goods.

The form can be generated both in electronic format and transferred on paper.

If the last day for filling out the document turns out to be non-working, then the deadline is postponed to the next weekday. Receiving money as an advance payment also involves the creation of an appropriate invoice.

There are cases when the seller can create at the end of the month one document for all products sold, this is possible if the company's activities involve constant sales to one buyer. Examples of this type of activity are the daily supply of products or the sale of communication services.

Such a seller prepares an invoice every month before the 5th day. In addition, one form for several sales documents can be generated if, within 5 days after the first sale, the seller has issued several more sales documents for this buyer. One invoice can be issued within five days.

AT retail, in the case of cash payment, VAT is not allocated as a separate line on price tags, checks and other forms, it is included in the cost, it is not required to create an invoice. In case of non-cash payment, an invoice will be required, but it can be issued in one copy at the end of the tax period.

Rules and features of filling out an invoice in 2019

A correctly drawn up document is the main requirement for subsequent accounting for the purpose of calculating VAT. The document has a certain form established by the state.

Formation of the invoice is divided into 2 parts:

- Creating a header for a document.

Here it is necessary to indicate the number of the document or its correction, the number of the payment document, the code and name of the currency in which the transaction takes place, data on the consignor and consignee. - Filling in the tabular section.

The tabular part is filled with information about the product, its unit of measurement, price and cost with and without tax, and the tax rate.

In this part, the name of the unit of measurement of the goods and its code from OKEI should be indicated, if such a unit is not in the classifier, then a dash is put.

When compiling, make sure that the name of the product is the same in all documents.

Line by line filling looks like this:

- 1 - number and date of the document;

- 2 - the name of the company selling the goods;

- 2a - address of the company;

- 2b - registration code;

- 3 - data on the consignor, if this is the seller, put "he";

- 4 - data on the consignee;

- 5 — information about the payment document;

- 6 - name of the company-buyer;

- 6a is the address of the company buying the product.

In the table in paragraphs 1 to 11, you must specify:

- 1 - the name of the goods;

- 2 - unit of their measurement;

- 3 - the number of goods sold;

- 4 - the price set by the sellers per unit of goods sold;

- 5 - calculated value without VAT;

- 6 - the amount of excise;

- 7 - tax rate;

- 8 - the amount of VAT on the entire volume of goods;

- 9 — cost with VAT;

- 10 - country of origin, it must be indicated if the goods are not of Russian origin;

- 11 - number of the declaration received at customs.

The document is signed by the head and accountant. There may be no last signature if the company's staffing table does not imply such a position.

Electronic invoices: changes 2019

The obvious advantage of document management in electronic form is efficiency. If earlier it took a lot of time to exchange documents between companies located in different regions, then with the possibility of electronic exchange, it only takes a couple of minutes.

In addition, postage and stationery costs are significantly reduced.

Firms that decide to implement electronic document management should take into account that since April of this year, an order containing new rules for the exchange in electronic format has come into force. The previously published order regulating this area has become invalid.

According to the new government order:

- All forms are electronically certified by a qualified digital signature (QEDS).

The electronic digital signature has been replaced by a qualified analogue for quite a long time, now this is reflected in the law. - Now it is not required to send a receipt notice, but if necessary, such a notice can be sent to the seller.

- Now you can send additional data to the invoice;

- The amendments to the Code provide for a change in the concepts of electronic invoicing, instead of the term "invoice in electronic form" there will be an "invoice in electronic form".

Find out from the video whether it is possible to create one invoice for a number of services.

When to apply adjustment invoices

A corrective invoice is generated if the cost of products sold has changed.

It is required if the following has changed:

- prices of goods;

- the number of goods sold;

- prices and quantities at the same time.

It is important not to confuse the corrective document and the correction of the existing one. The first one is set if it is necessary to adjust the amount of tax liabilities, a correction can be made if gross errors or typographical errors were found in the drawn up document.

Errors can also be in correction forms, they are corrected in the same order as regular ones.

Cases in which a corrective invoice is required:

- The seller provides a discount that reduces the cost of goods.

- The buyer received the wrong quantity of the item.

- The buyer did not take into account and returned part of the sold.

- The value of the goods has increased according to the conditions of the seller, for example, if the price depends on the payment term.

- There was a markdown of goods due to product quality.

- Increased cost of work due to rising prices for materials.

Adjustment of tax liabilities does not always entail the formation of an adjustment document:

- accepting a low-quality product for return, the seller should not generate an adjustment document, in this case, the reverse sale procedure takes place, the buyer acts as a seller and generates a regular document;

- in the case of the return of previously accepted goods, the buyer independently creates the appropriate document.

The corrective invoice is created by the seller no later than 5 days after the creation of documents evidencing the change in value. It, like a simple invoice, is drawn up in two copies, on paper or in electronic form.

It is permissible to draw up one corrective document for several previously issued ones. There is no special procedure for registration in, therefore, the rules of ordinary registration should be applied to such documents.

Features of advance invoices

When receiving payment or partial payment for goods that will be sold later, the seller is obliged to create an advance invoice. An interesting situation develops if the products were shipped within five days after payment.

The opinions of the Ministry of Finance and the tax authorities differ in this case: the legislature issued several explanations stating that in this case one invoice can be issued. The tax authorities do not agree with this opinion and argue that it is categorically impossible to do so.

In this case, it is still better to listen to the opinion of the tax authorities so that you do not have to prove the opposite point of view in court.

The document is not created in the following cases:

- goods sold are not subject to VAT;

- goods sold are taxed at a zero rate;

- if the duration of the production of goods sold exceeds six months;

- companies exempt from VAT.

In general, the preparation of advance invoices is subject to the same rules as the formation of regular invoices, but there are some nuances:

- in the sections "consignee" and "consignor" you need to put a dash;

- it is obligatory to enter data on the settlement document, cash or bank, if the advance is provided in the form of a netting, a bill of exchange and other non-monetary options, then a dash is also put in the column;

- data on the price, quantity, origin of the goods sold are not filled in;

- the tax amount will be calculated by multiplying the amount of the advance by the estimated tax rate in the format 10/110 or 18/118.

If within one day the buyer gradually made an advance payment, then all these payments will be recorded in one document. If the invoice is issued after shipment, then it must list the numbers of all payment documents related to this advance payment.

Companies that receive advances from buyers for continuous deliveries, such as telecommunications firms, can issue an invoice at the end of the month, reducing the advance by the number of services provided.

How invoices are numbered from 2018

The invoice numbering format is not established, the company can independently accept it by fixing it in the accounting policy. The main condition is the uniqueness of the numbers and the assignment of their forms in a through increasing order. The purpose of a single numbering is to combat those who issue certain documents retroactively.

The new rules provide for a clear definition of cases that allow the use of compound numbers:

- the document is exhibited by a separate subdivision;

- the sale was made by a trustee or a member of a simple partnership.

Although this will not cause a refusal to deduct, it is better not to use a dividing line in other cases.

Since there is no special form of advance invoices, they are numbered for all invoices in the company. If necessary, advance forms can be added letter designation as prefix AB.

For incorrect numbering of any criminal or administrative responsibility in the legislation is not provided.

An invoice is generated for each document for the sale of goods subject to VAT. Legislative acts imply strict requirements for filling and numbering.

Proper completion of this document will help the buyer to deduct tax, so it is important to know and understand the basic rules for its formation.

If it is necessary to adjust tax liabilities, an adjustment document can be issued, the preparation of which also has certain rules.

What is an invoice, why you need it, you can learn from the video.

In contact with

The invoice for services - a sample filling for 2019-2020 is presented in our article - is the object of close attention of controllers, and, accordingly, of many VAT payers engaged in activities of this kind. Consider what are the features of the design of this document on services.

Who should prepare invoices for services

NOTE! In 2019, e-invoices need to update the .

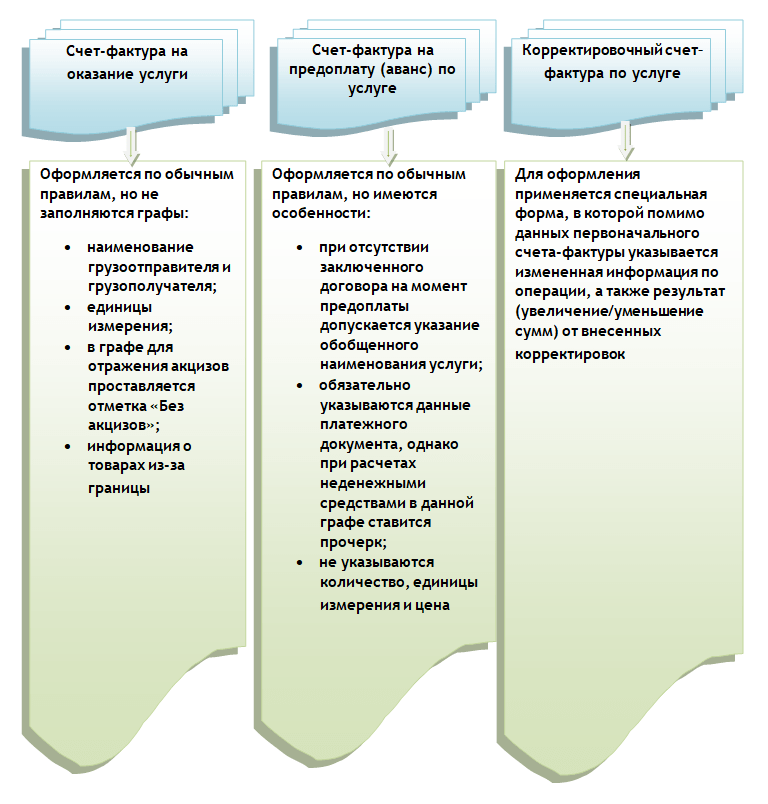

The specifics of issuing invoices for services is that some of these details are either not filled out at all, or allow some deviations from general rules, i.e.:

- It is not necessary to give the names of the shipper and the consignee (a dash is put), since in this case no products are shipped (subparagraphs “e”, “g”, paragraph 1 of section II of Appendix 1 to the Decree of the Government of the Russian Federation dated 26.12. 2011 No. 1137).

- When it is difficult to define a specific unit of measure for a service, it may be omitted. In this case, dashes should be put in the corresponding columns. If the unit is nevertheless determined, its name must be taken from the classifier OK 015-94 (MK 002-97).

- Excises for services in the Russian Federation are not legally established, therefore, in the corresponding column there will be an entry: “Without excise”.

- Data on goods imported from abroad are not filled in the document on services (we put dashes).

The name of the service appearing on the invoice must correspond to that specified in the contract for its provision (letter of the Ministry of Finance of Russia dated July 26, 2011 No. 03-07-09 / 22).

A sample of filling out an invoice for services in 2019-2020 can be downloaded on our website.

Completing invoices for prepaid amounts for services

There are few fundamental differences in filling out a document drawn up upon the provision of a service and an advance invoice:

- in the advance invoice, a generalized name of the service can be given if the agreement between the supplier and the buyer, from where the Ministry of Finance of Russia prescribes to take this name, has not been signed by that time;

- the advance invoice must necessarily reflect the number of the document confirming the fact of receipt of the prepayment, but if it is received in non-monetary form, a dash is put;

- when forming an advance invoice, there is no need to indicate the volume of services provided, their units of measurement, as well as their prices.

Thus, when forming an advance invoice for services, you can put dashes everywhere, except for the points that contain:

- number and date of the document;

- the names of the seller and the buyer, their TIN, addresses;

- number of the document confirming the advance payment;

- service name;

- currency name;

- prepayment amount;

- tax rate;

- the amount of VAT that is presented to the buyer.

IMPORTANT! The tax rate should be indicated in the advance invoice for services as 20/120 (18/118 - for advances received before 01/01/2019) or 10/110, and not as usual for many taxpayers 20 (18) or 10% (p 4 article 164 of the Tax Code of the Russian Federation).

Completing a corrective invoice for services

The corrective invoice for services should reflect:

- the exact title of the document (i.e. "Adjustment Invoice");

- number and date of compilation;

- numbers and dates of formation of invoices, according to which the cost or volume of services provided is adjusted;

- names of the seller and buyer, their addresses, TIN;

- names of services for which prices are adjusted or volume indicators are clarified;

- volume indicators of services (if any) before and after adjustments;

- the name of the settlement currency;

- government contract identifier (if any);

- price per unit of measurement of the service;

- the cost of the services provided without VAT - before and after price adjustments, volumes of services;

- tax rate;

- VAT amount - before and after adjustments;

- the cost of services provided, including VAT — before and after adjustments;

- the difference between the figures in the original invoices and those obtained as a result of adjustments.

Oh oh the differences between the corrective and corrected invoice, read the article “When is a corrected invoice used?” .

What VAT rate to indicate in the adjustment invoice from 2019, see.

Results

Invoices in connection with services are drawn up by VAT payers, using all 3 types of this document: main, advance, adjustment. The specificity of reflecting data on services in them lies in the fact that not all of their details are required to be filled in.

We advise you to read

Psychological characteristics of children in adolescence

Psychological characteristics of children in adolescence Transferring a child to another school - the procedure and necessary documents Whether to transfer a child to another school

Transferring a child to another school - the procedure and necessary documents Whether to transfer a child to another school, diagnosis, treatment Treatment of urogenital chlamydia") Chlamydia urogenital - description, causes, symptoms (signs), diagnosis, treatment Treatment of urogenital chlamydia

Chlamydia urogenital - description, causes, symptoms (signs), diagnosis, treatment Treatment of urogenital chlamydia The benefits and significance of hydroamino acid threonine for the human body L threonine what

The benefits and significance of hydroamino acid threonine for the human body L threonine what