In the accounting policy, you can configure the methods for calculating standard deductions. To set up deductions, in the Settings section, select Organizational details, go to the Accounting policies and other settings tab and click on the Accounting policies link at the bottom of the form.

You can set the use of tax deductions in 1C ZUP 8.3:

- Cumulative total – all deductions and income for the year are analyzed. If for a certain period an employee has no income, but the employment relationship does not terminate, then at the moment income appears for all previous periods in which the income was zero, deductions will be provided. But not more than the amount of income generated;

- Within the limits of monthly income - income for the month is analyzed; if there is no income, there is no deduction:

How to set up the procedure for applying standard tax deductions in 1C ZUP in accordance with the law is discussed in our video lesson:

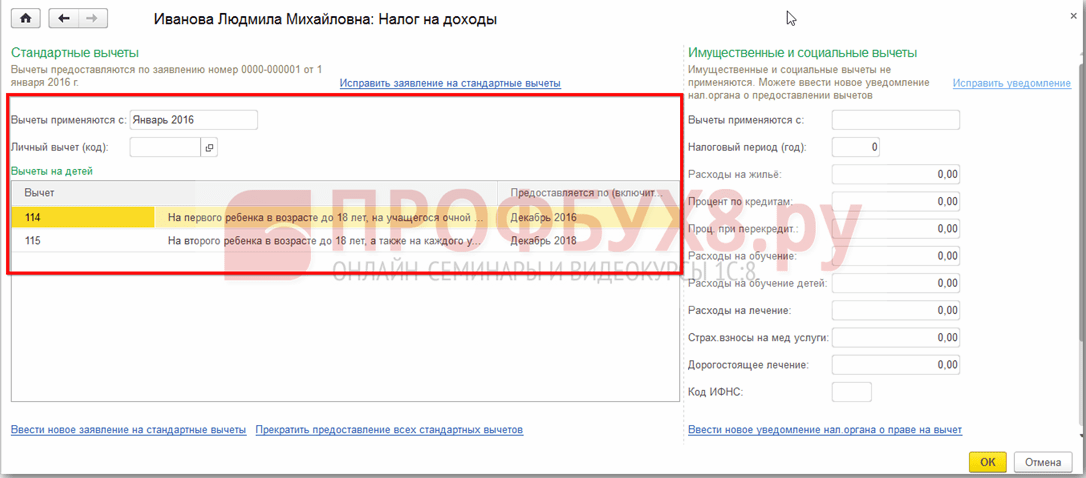

You can register the right to deduction in 1C ZUP 8.3 in the Taxes and Contributions section, then Application for Deductions and select Application for Deduction for Personal Income Tax:

You can also go to the Income Tax hyperlink from the employee’s card and select the Enter a new application for standard deductions link:

- Employee – filled in automatically if you enter a document from the “Employees” directory;

Important! It is impossible to enter several identical deductions for one period for one person, even if he works in several positions. This is controlled by individuals.

- Month – the month from which deductions are applied;

- Fill out the required deductions. In the document, it is possible to immediately issue a deduction for children in combination with a personal deduction or one of the types of deduction:

Deductions for children

When registering deductions for children in 1C ZUP 8.3, you must check the box in the document in the Change deductions for children field.

In the tabular part:

- Deduction – select the required deduction from the proposed list. The table displays the code line by line, and the adjacent column is automatically filled in with the deduction decoding;

- Provided by – the last month of the year of deduction expiration is indicated. Let’s say when a child turns 18;

- Documents – a document providing the basis for providing a deduction, for example, a certificate of education or birth certificate, as well as an employee’s statement:

Important! In 2016, a deduction for children is provided until the taxable income does not exceed 350,000 rubles. Until 01/01/2016 the limit was 280,000 rubles.

The amount of personal income tax deductions, the income limit, as well as the date from which they are valid can be viewed in the information register Amount of personal income tax deductions using the All functions menu item:

Personal deduction

To register a personal deduction in 1C ZUP 8.3, you must check the box Change personal deduction and select the required deduction code.

Important! Preferential deductions do not depend on income. And only one maximum deduction is provided.

It is also necessary to enter supporting documents in the Document confirming the right to personal deduction field:

Standard deductions for non-year-to-date employment

To correctly calculate deductions in 1C ZUP 8.3 when finding employment in the middle or end of the year, you must enter income from your previous place of work.

These incomes are entered from the employee’s card: section Personnel - directory Employees - click on the link Income Tax - further Income from the previous place of work:

For each month from the beginning of the year until employment, enter taxable income according to the 2-NDFL certificate:

Current deductions can be viewed in the employee’s card using the Income Tax hyperlink. You can also submit new documents to change or terminate the provision of standard deductions here:

To correct the application for standard deductions in 1C ZUP 8.3, you must use the link Correct the application for standard deductions. New change documents are entered using the Enter a new application for standard deductions link:

In the new document, you can change deductions or add new standard deductions:

When calculating wages in 1C ZUP 8.3, the personal income tax tab automatically displays all tax deductions that apply in the month of accrual. More detailed information on the calculation can be viewed via the link. For more details, see the Personal Income Tax Register:

This register describes what standard deductions an employee is entitled to:

As well as calculation of the tax base taking into account deductions:

Important! The amount of taxable income can be viewed in the personal income tax register, but it must be taken into account that the calculation does not display income from previous jobs, but when calculating deductions, they participate and are indicated in paragraph 3:

Termination of standard deductions in 1C ZUP 8.3

When dismissing an employee, in 1C ZUP 8.3 you must enter a special document Cancellation of standard personal income tax deductions. This document can be created from the Taxes and Contributions – Application for Deductions section or from an employee’s card in the same way as registering deductions, only by selecting the Stop providing all standard deductions link.

Important! Also, the document Cancellation of standard personal income tax deductions must be entered if the employee has written an application to terminate deductions in connection with receiving them at another enterprise.

Filling out the document:

- When you select an employee, the document is automatically filled in with all available standard deductions for the employee. If created from an employee card, the document is automatically completely filled out;

- You only need to set the month from which all standard deductions stop:

One of the standard tax deductions is a deduction for the taxpayer, which is provided to certain individuals, for example, Chernobyl victims, disabled people since childhood, parents and spouses of deceased military personnel. A complete list of individuals who may qualify for a standard deduction is indicated in paragraphs. 1, 2, 4 Article 218 of the Tax Code of the Russian Federation.

Taxpayers eligible for more than one standard deduction are allowed the maximum of the applicable deductions. In this case, the deduction for children is provided regardless of the provision of other standard tax deductions.

Types of standard tax deductions

Standard tax deductions:

tax deduction

This type of standard tax deduction is provided to 2 categories of individuals listed in paragraph 1 of Art. 218 Tax Code of the Russian Federation.

deduction for child(ren)

A deduction for a child (children) is provided up to the month in which the taxpayer’s income taxed at the rate 13%

and calculated on an accrual basis from the beginning of the year, exceeded 350,000 rubles. The deduction is canceled from the month when the employee’s income exceeds this amount.

- for the first and second child – 1400 rubles;

- for the third and each subsequent child – 3,000 rubles;

- for each disabled child under 18 years of age, or a full-time student, graduate student, resident, intern, student under the age of 24, if he is a disabled person of group I or II - 12,000 rubles for parents and adoptive parents (6,000 rubles for guardians and trustees).

If spouses, in addition to a common child, have a child from an early marriage, the common child is considered the third.

Procedure for obtaining a tax deduction for a child (children)

Provided to taxpayers who support a child (children).

Write an application for a standard tax deduction for a child (children) addressed to the employer.

Prepare copies of documents confirming the right to receive a deduction for the child (children):

- birth or adoption certificate of a child;

- certificate of disability of the child (if the child is disabled);

- a certificate from the educational institution stating that the child is a full-time student (if the child is a student);

- document confirming the registration of marriage between parents (passport or marriage registration certificate).

If the employee is the only parent (the only adoptive parent), it is necessary to supplement the set of documents with a copy of the document certifying that the parent is the only one.

If the employee is a guardian or trustee, it is necessary to supplement the set of documents with a copy of the document on guardianship or trusteeship of the child.

- resolution of the guardianship and trusteeship body or an extract from the decision (resolution) of the said body on the establishment of guardianship (trusteeship) over the child;

- agreement on the implementation of guardianship or trusteeship;

- agreement on guardianship of a minor citizen;

- foster family agreement.

Contact the employer with an application for a standard tax deduction for the child (children) and copies of documents confirming the right to such a deduction.

To correctly determine the amount of the deduction, it is necessary to line up the children according to their dates of birth. The first-born child is the oldest child, regardless of whether a deduction is provided for him or not.

If a taxpayer works for several employers at the same time, the deduction at his choice can be provided only with one employer.

An example of calculating the amount of tax deduction for children

Matveeva E.V. four children aged 16, 15, 8 and 5 years.

Moreover, her monthly income (salary) is 40,000 rubles.

Matveeva E.V. submitted a written application to the employer to receive a standard tax deduction for all children: for the maintenance of the first and second child - 1,400 rubles each, the third and fourth - 3,000 rubles per month.

Thus, the total tax deduction amounted to 8,800 rubles per month.

Every month from January to August the employer will pay his employee Matveeva E.V. Personal income tax from the amount of 31,200 rubles, received from the difference in income taxed at a rate of 13% in the amount of 40,000 rubles and the amount of tax deduction in the amount of 8,800 rubles:

Personal income tax = (40,000 rubles – 8,800 rubles) x 13% = 4,056 rubles.

Thus, in the hands of Matveev E.V. will receive 35,944 rubles.

If Matveeva E.V. did not apply for a deduction and did not receive it, then the employer would calculate personal income tax as follows:

Personal income tax = 40,000 rubles. x 13% = 5,200 rubles, income minus personal income tax would be 34,800 rubles.

In some cases, for example, for a single parent, the deduction amount may be doubled. At the same time, the parents being divorced and failure to pay child support does not imply the absence of a second parent for the child and is not a basis for receiving a double tax deduction.

Procedure for obtaining a tax deduction if during the year standard deductions were not provided by the employer or were provided in a smaller amount

If during the year standard deductions were not provided by the employer or were provided in a smaller amount, the taxpayer has the right to receive them when filing a personal income tax return with the tax authority at his place of residence at the end of the year.

In this case, the taxpayer must:

Obtain a certificate from the accounting department at your place of work about the amounts of accrued and withheld taxes for the corresponding year in form 2-NDFL.

Prepare copies of documents confirming the right to receive a deduction for the child (children).

Submit to the tax authority at your place of residence a completed tax return with an application for a standard tax deduction and copies of documents confirming the right to receive a standard tax deduction.

* If the submitted tax return calculates the amount of tax to be refunded from the budget, submit an application for a tax refund to the tax authority (together with the tax return, or after completing a desk tax audit).

The amount of overpaid tax is subject to refund upon application of the taxpayer within one month from the date the tax authority receives such an application, but not earlier than the end of the desk tax audit (Clause 6, Article 78 of the Tax Code of the Russian Federation).

When submitting copies of documents confirming the right to deduction to the tax authority, you must have their originals with you for verification by a tax inspector.

To enter information, you need to open the “Individuals” directory, which is located on the “Enterprise” tab.

Or you can go to the “Employees” directory and click on the link “More details and individuals...”.

In the form of the selected individual, click the “Personal Income Tax” button located on the top panel.

A window with three tables opens. In the upper left table, enter information about the right to personal deductions. Until 2012, all employees of the organization were provided with a personal deduction in the amount of 400 rubles (code 103), but it has now been canceled, therefore in this table it is possible to register the right only to provide a monthly deduction of 500 rubles (code 104) or 3000 rubles (code 105 ). However, these deductions are provided only to certain categories of citizens (Heroes of the Soviet Union and the Russian Federation, disabled people of groups I and II, victims during the liquidation of accidents at nuclear facilities, etc.), a complete list of which is contained in Art. 218Tax Code of the Russian Federation.

The top right table records information about eligibility for the standard deduction for children. A new line is added by clicking the "Add" button; you must indicate the period from which the deduction is provided (this can be the date the employee starts working or the date of birth of the child), and the first day of the corresponding month is indicated. You can also indicate the end date of the deduction period (the child reaches a certain age or completes full-time studies at a university), but you can leave this field empty. Information about each child is entered on a new line and each has a separate deduction code (for the third and subsequent children, one line is used, which simply indicates the number of children). The deduction for the first and second child is 1,400 rubles (codes 114 and 115), the deduction for the third and subsequent children is 3,000 rubles (code 116). For example, for an employee with four children, the table will be filled out as follows (in this case, deductions are provided for all children).

Also, separate codes are provided for double deductions (to a single parent, etc.), a list of codes with a description is available for selection in this table.

It is also necessary to fill out the bottom table of this form. It indicates which organization the deductions should apply to. This information is necessary in the case when an employee works simultaneously in several companies or leaves one organization and gets a job in another. But even if you keep records for only one organization, this information must still be provided, otherwise deductions will not be applied.

Deductions are provided for children until the cumulative taxable annual income does not exceed 280 thousand rubles. You can view information about the current amount of income in the employee’s payslip, which is located on the “Payroll” tab. Here you can also see information about the amount of deductions applied in the selected month.

Hello dear blog readers. We started a detailed conversation about personal income tax accounting in 1C ZUP and looked at the simplest example, which presented the full cycle of personal income tax accounting (by the way, you can read about the formation of 6-personal income tax in the article). In that example, personal income tax was calculated using the “Payroll” document. Today I will tell you in what other documents it is possible to calculate personal income tax, and we will also talk about what parameters are available in the 1C Salary and Personnel Management program for setting up personal income tax accounting, why they are needed and where they are located. In particular, we will discuss personal income tax deduction settings, as well as possible options for choosing the status of an individual for personal income tax accounting purposes ( resident, non-resident, highly qualified foreign specialist and others). In this article we will look at two examples:

- In the first one, we will work with the deduction settings - the employee has 4 deductions;

- In the second example, let's see how the program reflects and compensates for excessively withheld personal income tax when the taxpayer's status changes.

✅

✅

So, in the previous publication an example was presented where an employee had only one planned type of accrual, which was calculated in the document "Payroll" and personal income tax from this accrual was also calculated in the same document. But in 1C ZUP there are also a number of accrual documents that provide for the calculation of personal income tax. Let me first list all these documents:

- – “Payment” tab;

- – tab “Calculation of sick leave” -> “Personal income tax”

- – “NDFL” tab

The ability to calculate personal income tax in these documents appeared not so long ago. Previously, personal income tax was calculated only in document "Payroll" and that's why it should have been a last resort so that all accruals for the month are taken into account to correctly calculate personal income tax. This recommendation should still be followed now. Since most of the accrual documents still do not support the independent calculation of personal income tax, the amounts for these documents will be taken into account when calculating personal income tax in the final document “Payroll.” These include the following documents:

- Employee bonuses;

- Registration of downtime of employees of organizations;

- Calculation of severance.

Setting up personal income tax deductions in 1C ZUP

✅

✅ CHECKLIST for checking payroll calculations in 1C ZUP 3.1

VIDEO - monthly self-check of accounting:

✅ Payroll calculation in 1C ZUP 3.1

Step-by-step instructions for beginners:

Now let's talk about how the program sets up accounting for standard tax deductions. First, let me remind you what a tax deduction is. A tax deduction is a certain amount that reduces the tax base, i.e. not subject to personal income tax. In essence, this is a benefit established by the state for a certain circle of citizens. This is where I started talking about standard tax deductions. These include:

- 1400 rub. – for each child (for the first and second child) – code 114/108 (for the first child) and code 115 (for the second child);

- 3000 rub. – for the third and each subsequent child – code 116;

- 3000 rub. – for each disabled child of group I or II – code 117/109;

- 500 rub. - for persons with state awards: in particular, for Heroes of the Soviet Union, Heroes of Russia, for those awarded the Order of Glory of three degrees and many others - code 104 (in the ZUP this deduction is considered a personal standard deduction);

For those who are just starting to get acquainted with the theory of payroll calculation, accounting for personal income tax and deductions, I will give a small example. Let's assume that employee Stepanova has four children, i.e. she has the right to 2 deductions of 1400 rubles each. (code 114 and 115) and 2 deductions of 3000 rubles each. for the third and fourth child (code 116). She also has a salary of 30,000 rubles. Under these conditions, personal income tax (13%) will be calculated using the following formula: (30,000 – (1,400 + 1,400 + 3,000 + 3,000)) * 13% = 21 200 * 13% = 2,756 rub. Thus, the tax base will not be the entire salary, but the amount reduced by the amount of deductions due.

Let's now implement this example in the 1C ZUP program. To fill out information about an employee’s right to standard deductions, the program uses the “Data Entry for Personal Income Tax” form. It can be accessed from the “Employees of the Organization” directory form.

You can also fill in the Reason field, but this is not required. If the Deduction is terminated, the Date and status are indicated "do not apply".

In our example, the employee does not have personal deductions, so we will leave this tabular part empty.

The second tabular part in this form is called "Eligibility for Standard Deduction for Children". We will fill out this form for employee Stepanova. Let me remind you that, according to the conditions of the example, she has four children and, accordingly, can use the following deductions:

- 114/108 – for the first child 1,400 rubles;

- 115 – for the second child 1,400 rubles;

- 116 – for the third and fourth child, 3,000 rubles each. for everyone;

The fields in this tabular section are approximately the same. The only difference is that you can indicate the number of children (we use this option for deduction code 116) and indicate the date until which the deduction is valid, if this is known in advance (we use this for deduction 114/108). You can also stop deduction by entering a separate line, indicating the value “Do not apply”, deduction code and date. The screenshots show both options.

Another tabular part in this form is called "Application of deduction".

And this you need to do it even if you have one organization in the program, otherwise deductions will not be taken into account.

I would also like to draw your attention to the fact that there is another bookmark in this form. Let me remind you that the standard tax deduction is applied until the employee’s cumulative income from the beginning of the year does not exceed 280,000 rubles. Therefore, if an employee does not join the organization from the beginning of the year, then for him you should indicate the income that he had in the previous or previous organization from the beginning of the year. This data will only be taken into account to track the RUB 280,000 limit. These amounts will not affect the calculation of average earnings in any way.

In our case, the employee was hired at the beginning of the year and therefore bookmark “Income from previous jobs” leave it blank.

Taxpayer status for personal income tax

✅ Seminar “Lifehacks for 1C ZUP 3.1”

Analysis of 15 life hacks for accounting in 1C ZUP 3.1:

✅ CHECKLIST for checking payroll calculations in 1C ZUP 3.1

VIDEO - monthly self-check of accounting:

✅ Payroll calculation in 1C ZUP 3.1

Step-by-step instructions for beginners:

Taxpayer status in 1C ZUP can be established using the form “Data entry for personal income tax”. It can be opened from the form of the “Employees” directory element in the “Status” field. There are 5 options to select the status:

- Resident

- Non-resident

- Highly qualified foreign specialist

- Participant in the program for the resettlement of compatriots

- Refugee or who has received temporary asylum on the territory of the Russian Federation - appeared in the release of ZUP 2.5.85

There are explanations in the program for each option, so I will only focus on the features of reflecting the situation when an employee’s status changes in the middle of the year. As you can see, in addition to the switches themselves, the form has a field where the period is set. Those. this indicator is periodic. Let's look at a similar situation.

An employee who is a foreign citizen and at the time of hiring (01/10/2014) resides in the Russian Federation is hired by the organization. less than 183 calendar days. Therefore, he is given the status "Non-resident". As a result, personal income tax for January and February is calculated at a rate of 30%.

It turns out that the employee’s personal income tax for January and February is 18,000 = 9,000 + 9,000 = 30,000 * 30% + 30,000 * 30%.

In March, the deadline comes when a foreign citizen’s stay on the territory of the Russian Federation will exceed 183 days. Therefore he acquires the status "Resident". In this case, in 1C it is necessary to change the employee’s status indicating the month in which he received the corresponding status and this will be saved in the history of changes.

As a result, the employee’s personal income tax will begin to be calculated at a rate of 13% from March. But this is not the only change that will occur. When calculating personal income tax for March, the tax for January and February will be recalculated at a rate of 13%. Negative amounts will be calculated for January and February: 30,000 * (13%-30%) = -30,000 * 17% = - 5100; -5,100 *2 = -10,200 rub. (excess withheld for 2 months).

Refunds of excess withheld amounts will be made from the tax calculated in March: RUB 3,900. Those. in March, the employee will receive his full salary without personal income tax withholding. However, personal income tax for March is not enough to fully compensate for the excessively withheld amount and therefore in the pay slip for March in the line “including: excessively withheld personal income tax at the end of the period” we will see the figure 6,300 = 10,200 (the amount of excess withheld at the beginning of March) - 3,900 (returned from the March personal income tax).

Please note that this debt in the amount of 6,300 rubles. Although it is listed as a debt for the organization, it will not affect the amount of salary payable. The employee will be paid 30,000, not 36,300.

Thus, the return of excessively withheld personal income tax to the employee will be carried out in the next two months, at the expense of the calculated personal income tax in these months. I hope I explained this mechanism clearly.

In this example, we have a rather simple situation: the employee’s status changed at the beginning of the year and there is time to compensate for personal income tax due to the following months. But it may turn out that the employee changes status, for example, in November and simply there won't be enough time until the end of the year to compensate the entire excess amount withheld. In this case, the program will not carry over this debt to the next year. The employee should independently contact the tax office and it will be the one who will return the excess withheld funds to him. In this case, you should not enter the document “Personal income tax return”, since the tax agent (the employer is the tax agent for the payment of personal income tax) does not have the right to return personal income tax to the employee, but can only offset the overpaid amounts against the following months (I talked about this a little higher with an example).

That's all for today!

To be the first to know about new publications, subscribe to my blog updates: